Why Higher Rates Are Actually a Tailwind for KC

Most people hear "higher-for-longer" and assume it's bad news across the board. For supply-constrained markets, it's the opposite.

Higher financing costs make new development harder to pencil and capitalize in most markets. That means fewer new development starts. Fewer starts mean less new supply coming online in 2027, 2028, even 2029.

Markets that were already tight get tighter. Subsequently rents continue to move up. The cash flow thesis only gets stronger with market capital constraints.

For the Bucket 3 markets, the dynamic is uglier. Sponsors on floating rate debt can't refinance. Insurance keeps climbing. Property tax assessments induce panic attacks. The margin doesn't ease, and the growth headlines just aren't enough to cover the structural costinflation.

That's the difference between a cyclical correction and a structural problem. And it's why where you invest matters as much as what you invest in.

The Reserve at Copper Creek: Proof of Concept

We broke ground on The Reserve at Copper Creek in Lenexa, Kansas at the end of 2025. Vertical construction is underway right now. Hold your applause... but, it's kind of a big deal.

And the numbers at the project level tell the full Kansas City story.

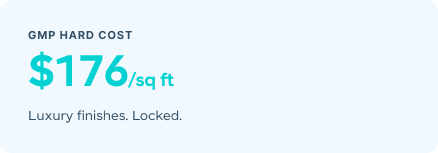

Hard costs for luxury multifamily in Kansas City are running $175–$250 per square foot. Our GMP contract on The Reserve at Copper Creek came in at $176. Across most coastal gateway markets, the same product costs $300, $350, $380 or more per square foot. In many cases, those markets are delivering lower rents per square foot than Kansas City right now, due to elevated vacancy and concession pressure.

The math creates a margin of safety that simply doesn't exist in overheated markets. You're building at a lower cost basis. You're delivering into a market with less competitive supply. And you're capturing rent premiums in a submarket, Johnson County, that attracts exactly the high-income renter who wants a luxury product and will pay for it.

.svg)

.png)

.png)

.png)